AI Builder Market Competitive Landscape and Future Growth Trends

Music |

2026-06-19 07:09:35

The Laminated Can Packaging Market is experiencing steady growth as industries increasingly adopt durable, lightweight, and visually appealing packaging solutions. Laminated cans are manufactured using multiple layers of materials such as paperboard, aluminum foil, and plastic films to provide enhanced protection against moisture, oxygen, and contaminants. Their superior barrier properties make them suitable for a wide range of applications, particularly in food, beverage, and pharmaceutical packaging. Growing demand for shelf-stable packaging and changing consumer lifestyles continue to support market expansion.

Request Sample Link:

https://packagingmarketinsights.com/report/laminated-can-packaging-market/request-sample

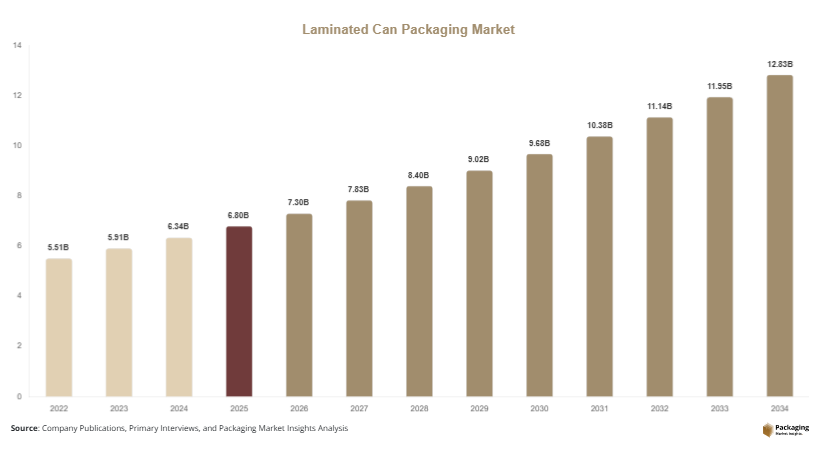

The laminated can packaging market size was valued at approximately USD 6.8 billion in 2025 and is projected to reach USD 7.3 billion in 2026. The market is further expected to expand to around USD 12.9 billion by 2034, growing at a CAGR of 7.3% during 2025–2034.

The market is gaining momentum as manufacturers seek packaging solutions that combine durability, lightweight construction, and attractive product presentation. Laminated cans offer excellent barrier protection, helping preserve product freshness and extend shelf life. Their increasing use across food, beverage, pharmaceutical, and other industries continues to strengthen market growth.

The Laminated Can Packaging Market demonstrates strong growth potential throughout the forecast period.

Market Size (2025): USD 6.8 Billion

Market Size (2026): USD 7.3 Billion

Forecast Market Size (2034): USD 12.9 Billion

CAGR (2025–2034): 7.3%

The market expansion is supported by increasing demand for packaged food products, advancements in packaging technologies, and growing adoption of sustainable packaging materials.

One of the primary drivers of the laminated can packaging market is the growth of the packaged food and beverage industry. Rising urbanization, changing lifestyles, and increasing disposable incomes are encouraging consumers to purchase convenient and ready-to-eat food products. Laminated cans help maintain freshness, preserve nutritional value, and extend product shelf life, making them a preferred packaging solution.

Another significant driver is the advancement in packaging technology. Continuous innovations in material composition and manufacturing processes have improved barrier performance, durability, and lightweight characteristics of laminated cans. Production automation has also increased manufacturing efficiency while reducing costs, enabling companies to meet evolving customer requirements and regulatory expectations.

A major challenge facing the laminated can packaging market is the complexity of recycling laminated materials. Since laminated cans consist of multiple material layers, separating these materials during recycling can be difficult.

The combination of plastic, aluminum, and paper layers creates challenges for recycling systems, limiting recyclability and increasing environmental concerns. Although manufacturers are investing in recyclable laminated structures, the associated technological complexity and development costs may slow broader market adoption.

Emerging markets present substantial opportunities for the laminated can packaging market. Rapid urbanization and industrial development across Asia Pacific, Latin America, and the Middle East are increasing demand for packaged consumer goods. Rising purchasing power is encouraging greater adoption of high-quality and convenient packaging solutions, creating favorable market conditions.

Another promising opportunity lies in the development of innovative and smart packaging solutions. Technologies including QR codes, NFC tags, and interactive packaging features are being incorporated into laminated cans to improve consumer engagement and provide additional product information. These innovations help manufacturers differentiate their products while enhancing customer experience.

Composite laminated cans dominated the market with approximately 34.5% market share. Their superior barrier protection and structural strength make them suitable for food, beverage, and pharmaceutical applications.

Eco-friendly laminated cans are projected to witness the fastest growth with a CAGR of 8.1% during the forecast period, supported by increasing emphasis on sustainable packaging materials.

Paper-based laminated packaging accounted for approximately 51.8% of the market due to its recyclability, cost-effectiveness, and support for sustainability initiatives.

Biodegradable materials are expected to grow at a CAGR of 7.4% during the forecast period as manufacturers increasingly adopt environmentally friendly packaging alternatives.

Food & beverage remained the largest application segment with a market share of approximately 46.7%. Growing demand for packaged food products continues to support this segment.

Pharmaceutical packaging is anticipated to register the fastest CAGR of 7.8%, driven by increasing demand for reliable packaging solutions that protect products from moisture and contamination.

Asia Pacific dominated the laminated can packaging market with a 39.2% share in 2025 and is projected to maintain strong growth at a CAGR of 7.6%. Rapid urbanization, expanding food and beverage industries, and growth in e-commerce continue to support regional demand. China remained the leading country with a market size of USD 1.5 billion in 2025 and USD 1.6 billion in 2026.

North America accounted for approximately 28.7% of the market in 2025 and is expected to grow at a CAGR of 6.8%. The region benefits from a mature food and beverage industry and increasing adoption of sustainable packaging solutions. The United States remains the dominant country in the region.

Europe held around 25.3% of the market share in 2025 and is projected to grow at a CAGR of 6.7%. Germany leads the regional market, supported by advanced manufacturing capabilities and increasing demand for environmentally friendly packaging.

The Middle East & Africa represented approximately 3.8% of the market in 2025 and is forecast to grow at a CAGR of 6.5%. Growth is driven by increasing investments in food processing and modern retail infrastructure, with Saudi Arabia serving as a key contributor.

Latin America accounted for around 3.0% of the market in 2025 and is expected to grow at the fastest CAGR of 7.6%. Brazil leads the regional market due to its expanding food processing industry and increasing demand for convenient packaging solutions.

The laminated can packaging market is moderately competitive, with companies focusing on innovation, sustainability, and product development. Leading market participants include:

Sonoco Products Company

Amcor plc

Smurfit Kappa Group

Mondi Group

DS Smith Plc

Ball Corporation

Crown Holdings Inc.

Greif Inc.

The Laminated Can Packaging Market is expected to experience consistent growth through 2034, supported by increasing demand for packaged food, technological advancements, sustainable packaging initiatives, and expanding opportunities in emerging markets. Despite challenges associated with recycling laminated materials, ongoing innovation and smart packaging developments continue to create new opportunities across multiple industries.

With projected growth from USD 6.8 billion in 2025 to approximately USD 12.9 billion by 2034 at a CAGR of 7.3%, the Laminated Can Packaging Market is positioned for sustained expansion. Continued investments in sustainable materials, innovative packaging technologies, and regional market development are expected to support long-term industry growth.

Report Link:

https://packagingmarketinsights.com/report/laminated-can-packaging-market