Call Girl Bhubaneswar – 24 HRS Verified Bhubaneswar Escort Services!

Other |

2026-07-07 07:00:55

The global Rigid Polyolefin Market is witnessing steady growth as industries increasingly demand durable, lightweight, and cost-efficient plastic materials. Rigid polyolefins, primarily polyethylene (PE) and polypropylene (PP), are widely used across packaging, automotive, construction, and consumer goods due to their strength, chemical resistance, and versatility. The market is also benefiting from the growing preference for recyclable materials and the development of advanced polyolefin grades that support sustainability goals.

Request Sample Link:

https://packagingmarketinsights.com/report/rigid-polyolefin-market/request-sample

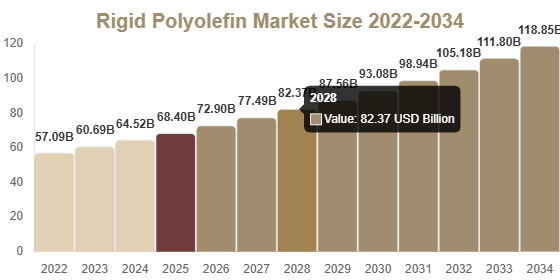

The global rigid polyolefin market size was valued at USD 68.4 billion in 2025 and is projected to reach USD 72.9 billion in 2026. Over the forecast period, the market is expected to reach approximately USD 126.3 billion by 2034, expanding at a CAGR of 6.3% from 2025 to 2034.

The increasing adoption of recyclable and circular polyolefin materials is reshaping the industry. Manufacturers are investing in advanced recycling technologies and mono-material packaging solutions to improve recyclability while maintaining product performance. At the same time, innovations in manufacturing processes such as injection molding, blow molding, and extrusion are enabling the production of lightweight yet durable products that meet the evolving needs of multiple industries.

The rigid polyolefin market demonstrates strong long-term growth potential.

Market Size (2025): USD 68.4 Billion

Market Size (2026): USD 72.9 Billion

Forecast Market Size (2034): USD 126.3 Billion

CAGR (2025–2034): 6.3%

The market's expansion is supported by growing demand across packaging, automotive, construction, and consumer goods industries. Continuous improvements in product performance and sustainability initiatives are expected to contribute to consistent market growth throughout the forecast period.

The rapid expansion of the packaging industry remains a primary driver of the rigid polyolefin market. Rigid polyolefins are widely used in packaging because of their durability, strength, and resistance to moisture and chemicals. The growth of e-commerce has increased the need for reliable packaging solutions that protect products during transportation, encouraging manufacturers to develop efficient and sustainable packaging materials.

The automotive and construction industries continue to generate significant demand for rigid polyolefins. In automotive applications, these materials help reduce vehicle weight while maintaining impact resistance, contributing to improved fuel efficiency. In construction, rigid polyolefins are extensively used in pipes, insulation, and structural components because of their durability and cost-effectiveness.

Environmental concerns and regulatory restrictions on plastic usage present major challenges for the rigid polyolefin market. Governments and environmental organizations are introducing policies to reduce plastic waste and encourage sustainable alternatives. This has increased scrutiny of polyolefin materials, particularly in single-use applications.

Manufacturers are investing in recycling infrastructure and developing environmentally friendly materials to comply with changing regulations. Restrictions on certain plastic products in various regions have also impacted market demand while increasing operational costs.

The development of bio-based and recycled polyolefins offers substantial opportunities for market growth. Manufacturers are exploring renewable feedstocks to produce materials with reduced environmental impact while maintaining performance characteristics comparable to conventional polyolefins.

Emerging economies present significant growth opportunities due to rapid urbanization and infrastructure development. Regions including Asia Pacific and Latin America are experiencing increasing demand for construction materials and consumer goods, supporting broader adoption of rigid polyolefins. Growing middle-class populations and rising consumer spending further contribute to market expansion.

Polypropylene accounted for the largest market share of 45.6%, supported by its versatility and broad range of applications across packaging, automotive components, and consumer goods. High-density polyethylene is projected to grow at a CAGR of 6.5% due to its strength, durability, and increasing use in containers, pipes, and industrial applications.

Other product types include:

Polypropylene

High-Density Polyethylene

Low-Density Polyethylene

Polyolefin Blends

Packaging represented the largest application segment with a 54.2% market share, driven by strong demand for lightweight and durable materials used in containers, bottles, and caps. Construction applications are forecast to grow at a CAGR of 6.1% owing to increasing infrastructure development.

Application segments include:

Packaging

Construction

Automotive

Consumer Goods

The market is segmented into:

Direct Sales (B2B)

Distributors & Wholesalers

Online Industrial Platforms

Specialty Chemical Suppliers

Retail Industrial Stores

Food & beverage remained the leading end-use segment with a 41.8% share due to increasing demand for packaged food products and the need to enhance product safety and shelf life. Automotive applications are expected to grow at a CAGR of 6.4% as manufacturers continue adopting lightweight materials for vehicle components.

Asia Pacific dominated the rigid polyolefin market with a 38.7% share in 2025 and is projected to grow at a CAGR of 6.9%. Rapid industrialization, urbanization, and increasing demand from packaging, automotive, and construction industries continue to drive regional growth. China remains the leading country, with a market size of USD 18.5 billion in 2025 and USD 19.7 billion in 2026.

North America accounted for 26.9% of the market share in 2025 and is expected to grow at a CAGR of 5.9%. Growth is supported by advanced manufacturing capabilities, strong packaging demand, and expanding e-commerce activities. The United States leads the regional market.

Europe held a 23.7% market share in 2025 and is projected to expand at a CAGR of 6.0%. The region benefits from strict environmental regulations, increasing adoption of recyclable materials, and strong demand from packaging and automotive industries. Germany remains the leading country in the region.

The Middle East & Africa accounted for 5.4% of the market share in 2025 and is anticipated to grow at a CAGR of 6.2%. Industrial expansion, infrastructure development, and strong petrochemical production support regional demand, with Saudi Arabia serving as a key market.

Latin America represented 5.3% of the market in 2025 and is projected to record the fastest regional CAGR of 6.8%. Rising consumer demand, expanding industrial sectors, improving infrastructure, and growing e-commerce activities are supporting market growth. Brazil leads the regional market.

The rigid polyolefin market is moderately competitive, with companies focusing on product innovation, sustainability, research and development, strategic partnerships, and portfolio expansion. Key market participants include:

ExxonMobil Corporation

LyondellBasell Industries N.V.

SABIC

Dow Inc.

INEOS Group

Borealis AG

Braskem S.A.

Formosa Plastics Corporation

The Rigid Polyolefin Market is expected to experience consistent growth throughout the forecast period, supported by increasing demand across packaging, automotive, construction, and consumer goods industries. Rising adoption of recyclable materials, advancements in manufacturing technologies, and expanding infrastructure development in emerging markets continue to create favorable growth opportunities. At the same time, manufacturers are addressing environmental concerns through investments in sustainable and recycled polyolefin solutions while adapting to evolving regulatory requirements.

With a market size projected to reach USD 126.3 billion by 2034 at a CAGR of 6.3%, the Rigid Polyolefin Market is positioned for sustained expansion. Continued innovation, strong industrial demand, and increasing emphasis on sustainability are expected to support long-term market development during the forecast period.

Report Link:

https://packagingmarketinsights.com/report/rigid-polyolefin-market