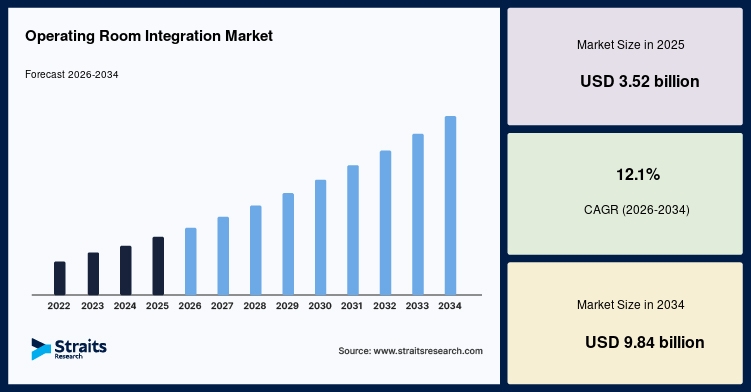

The global operating room integration market is witnessing robust growth due to increasing adoption of minimally invasive surgeries, rising investments in smart hospitals, growing demand for advanced surgical workflow management, and continuous advancements in digital healthcare technologies. The global operating room integration market size was valued at USD 3.52 billion in 2025 and is projected to grow from USD 3.95 billion in 2026 to USD 9.84 billion by 2034, registering a CAGR of 12.1% during the forecast period (2026–2034).

Operating room integration refers to the seamless integration of surgical equipment, imaging systems, audiovisual technologies, patient data, and communication platforms into a centralized digital environment. These systems enhance surgical workflow, improve communication among healthcare professionals, streamline data management, and support better clinical decision-making during surgical procedures. Increasing emphasis on patient safety, operational efficiency, and real-time information access continues to accelerate market growth.

Market Drivers

Rising Adoption of Minimally Invasive Surgeries

The growing preference for minimally invasive procedures is increasing demand for integrated operating rooms equipped with advanced imaging, visualization, and surgical navigation systems.

Expansion of Smart Hospitals

Healthcare providers are investing in digitally connected hospitals that utilize integrated operating room technologies to improve workflow efficiency and patient outcomes.

Increasing Demand for Surgical Workflow Optimization

Operating room integration solutions enable centralized control of medical devices, improve communication among surgical teams, and reduce procedure times.

Growing Healthcare Infrastructure Investments

Governments and private healthcare organizations are expanding hospital infrastructure and modernizing surgical facilities with advanced digital technologies.

Advancements in Medical Imaging and Visualization

Continuous innovations in high-definition imaging, 3D visualization, robotic surgery, and artificial intelligence are enhancing operating room integration capabilities.

For Detailed Insights, Visit:

https://straitsresearch.com/report/operating-room-integration-market

Market Challenges

High Installation and Implementation Costs

Integrated operating room systems require substantial investments in hardware, software, networking infrastructure, and installation services.

Complex System Integration

Integrating multiple medical devices, hospital information systems, and imaging platforms from different manufacturers can present technical challenges.

Data Security and Privacy Concerns

The increasing exchange of patient information across connected systems requires robust cybersecurity measures and compliance with healthcare data regulations.

Training Requirements

Healthcare professionals require specialized training to effectively operate advanced integrated surgical technologies and digital workflow platforms.

Market Segmentation

The operating room integration market is segmented based on component, application, end user, and region.

By Component

The market is categorized into:

-

Software

-

Hardware

-

Services

Hardware accounts for the largest market share due to increasing adoption of integrated displays, cameras, control panels, imaging systems, and audiovisual equipment.

By Application

The market includes:

-

General Surgery

-

Orthopedic Surgery

-

Neurosurgery

-

Cardiovascular Surgery

-

Thoracic Surgery

-

Gynecological Surgery

-

Others

General surgery dominates the market owing to the high volume of surgical procedures performed globally and increasing use of integrated operating room technologies.

By End User

The market is segmented into:

Hospitals represent the largest end-user segment due to extensive investments in advanced surgical infrastructure, digital operating rooms, and smart healthcare technologies.

By Region

The market is analyzed across:

-

North America

-

Europe

-

Asia-Pacific

-

Latin America

-

Middle East & Africa

Regional Insights

North America

North America dominates the operating room integration market due to advanced healthcare infrastructure, widespread adoption of minimally invasive surgeries, increasing investments in smart hospitals, and the presence of leading medical technology companies.

Europe

Europe holds a significant market share supported by healthcare digitalization initiatives, increasing surgical procedure volumes, government healthcare investments, and rapid adoption of advanced operating room technologies.

Asia-Pacific

Asia-Pacific is expected to witness the fastest growth due to expanding healthcare infrastructure, increasing healthcare expenditure, rising surgical volumes, and growing investments in hospital modernization across China, India, Japan, South Korea, and Southeast Asia.

Latin America

Latin America is experiencing steady market growth driven by improving healthcare facilities, increasing adoption of digital surgical technologies, and expanding private healthcare investments.

Middle East & Africa

The region is witnessing gradual growth owing to hospital expansion projects, rising healthcare investments, and increasing adoption of advanced surgical equipment.

Technology Trends and Market Opportunities

The operating room integration market is evolving through innovations in artificial intelligence-assisted surgery, robotic surgical platforms, cloud-based healthcare systems, 4K and 8K surgical visualization, Internet of Medical Things (IoMT), voice-controlled operating rooms, and augmented reality-assisted surgical navigation. Healthcare providers are increasingly integrating electronic health records (EHR), surgical imaging systems, and real-time data analytics to improve surgical precision and workflow efficiency.

Growing investments in robotic-assisted surgery, telemedicine, digital operating rooms, smart hospitals, healthcare automation, and connected medical devices are creating significant opportunities for market participants. Furthermore, increasing demand for remote surgical collaboration and data-driven healthcare solutions is expected to support long-term market growth.

Key Players Analysis

The operating room integration market is highly competitive, with leading medical technology companies focusing on integrated surgical platforms, digital workflow solutions, advanced visualization technologies, and strategic collaborations.

Major companies operating in the market include:

These companies continue to invest in intelligent operating room solutions, robotic surgery integration, advanced imaging technologies, and healthcare digitalization to strengthen their positions in the global operating room integration market.

Related Report

Operating Room Equipment Market

https://straitsresearch.com/report/operating-room-equipment-market

About Us

Straits Research is a leading market research and intelligence organization specializing in analytics, advisory services, and comprehensive market research reports across multiple industries.

Contact Us

Email: sales@straitsresearch.com

U.S. Tel: +1 646 905 0080

U.K. Tel: +44 203 695 0070