Internet of Everything Market Expansion Fueled by AI and 5G Integration 2030

Other |

2025-04-11 10:42:56

Upgrade auf Pro

The global 3D IC and 2.5D IC packaging market is witnessing significant growth as semiconductor manufacturers increasingly adopt advanced packaging technologies to support artificial intelligence workloads, high-performance computing, automotive electronics, and next-generation consumer devices. Rising demand for AI accelerators, high-bandwidth memory (HBM), and compact high-performance semiconductor architectures is accelerating investment in advanced packaging infrastructure worldwide.

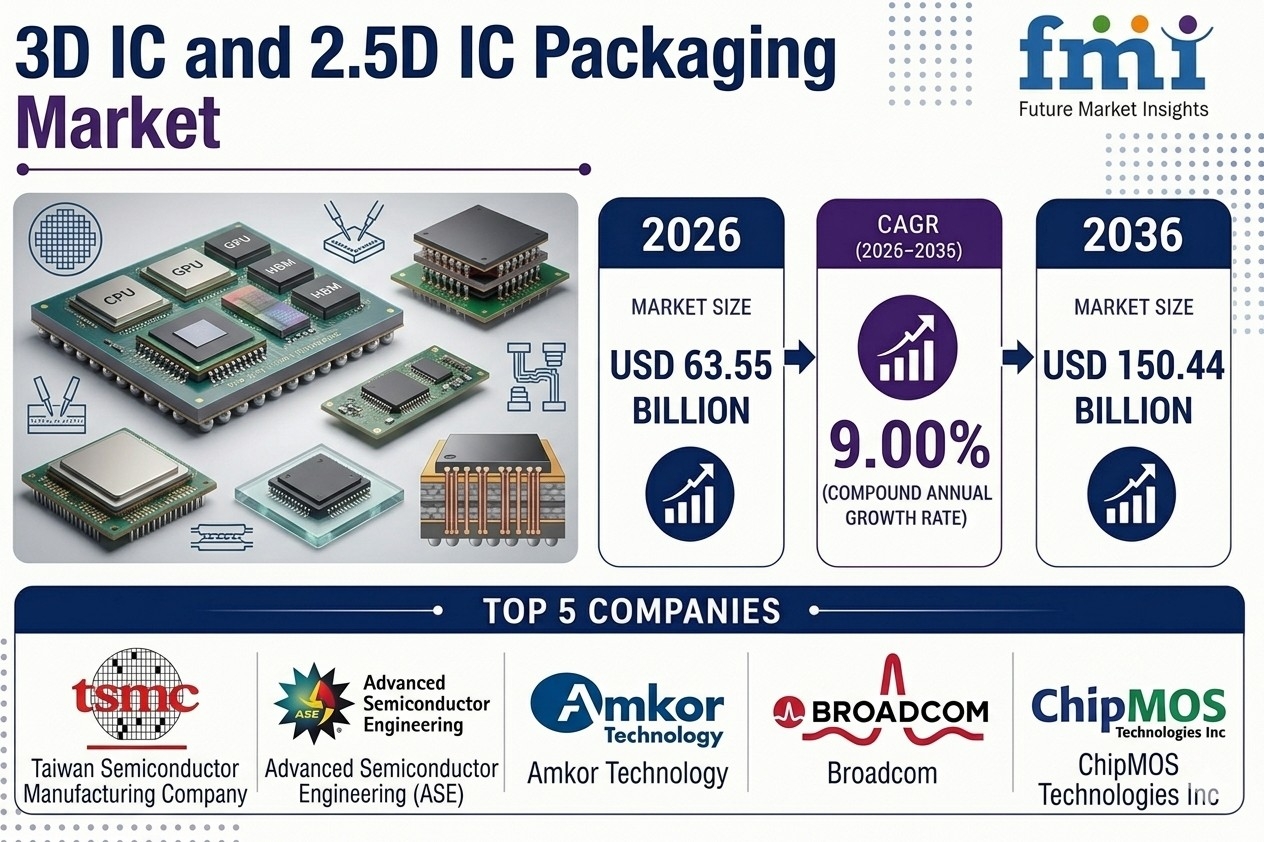

3D IC and 2.5D IC Packaging Market Snapshot

Get Detailed Market Forecasts, Competitive Benchmarking, and Pricing Trends: https://www.futuremarketinsights.com/reports/sample/rep-gb-25260

Market Overview

3D IC and 2.5D IC packaging technologies enable multiple semiconductor dies to be integrated into a single package using advanced interconnect architectures such as:

These technologies provide major advantages including:

The market is increasingly driven by the rapid expansion of AI infrastructure and advanced computing applications.

AI Accelerators Fueling Packaging Demand

Artificial intelligence workloads are becoming the largest growth catalyst for advanced semiconductor packaging.

Rising AI Chip Production

Leading AI chips including:

require advanced 2.5D packaging technologies such as:

These packaging solutions are essential for integrating high-bandwidth memory adjacent to logic processors.

Traditional 2D semiconductor packaging can no longer support the interconnect density and memory bandwidth requirements demanded by modern AI accelerators.

HBM Memory Driving TSV Adoption

3D TSV Technology Holds 50.6% Market Share

Through-silicon via (TSV) technology remains the dominant packaging technology because it enables vertical stacking of memory dies.

HBM manufacturers including:

are increasingly deploying TSV stacking technologies to support:

Each AI accelerator package typically requires multiple HBM stacks, creating massive demand for advanced TSV packaging capacity.

Key Advantages of TSV Technology

Advancements in TSV manufacturing are also improving production yields and reducing overall packaging costs.

Logic Applications Dominate Market Demand

Logic Segment Accounts for 45.9% Share

Logic applications remain the leading segment due to rising demand for:

Advanced packaging technologies allow logic chips to integrate memory and compute components within a single package, enabling:

The increasing complexity of AI and cloud computing workloads continues accelerating demand for advanced logic packaging solutions.

Consumer Electronics Remain Largest End-use Sector

Consumer Electronics Hold 38.4% Market Share

Consumer electronics remain the largest end-use industry because of strong demand for compact and high-performance devices including:

Electronics manufacturers increasingly rely on 3D and 2.5D packaging to deliver:

As consumer expectations continue rising, advanced packaging is becoming a critical differentiator in device performance.

Automotive Electronics Emerging as Major Opportunity

The automotive sector is rapidly adopting advanced semiconductor packaging technologies for:

Key Automotive Packaging Applications

Manufacturers are integrating:

into advanced heterogeneous 2.5D packages.

These systems require:

The growth of electric vehicles and autonomous driving technologies is expected to create substantial long-term opportunities for advanced packaging providers.

High-performance Computing Expanding Market Growth

The growth of cloud computing, AI data centers, and enterprise workloads is significantly increasing demand for advanced semiconductor packaging.

HPC and Data Center Requirements

Modern data centers require:

Advanced 3D IC and 2.5D packaging technologies help address these requirements while improving energy efficiency and integration density.

Key Technology Trends

Smart Manufacturing and Automation

Semiconductor packaging manufacturers are increasingly deploying:

These innovations improve:

Heterogeneous Integration

The market is rapidly moving toward heterogeneous integration where multiple chip types are combined within a single package.

This includes integration of:

Speak to Analyst: Customize insights for your Business Strategy: https://www.futuremarketinsights.com/customization-available/rep-gb-25260

Key Market Drivers