Thermal Interface Materials Market Forecast 2026–2036: Market Expansion Driven by Electronics Minisaturization

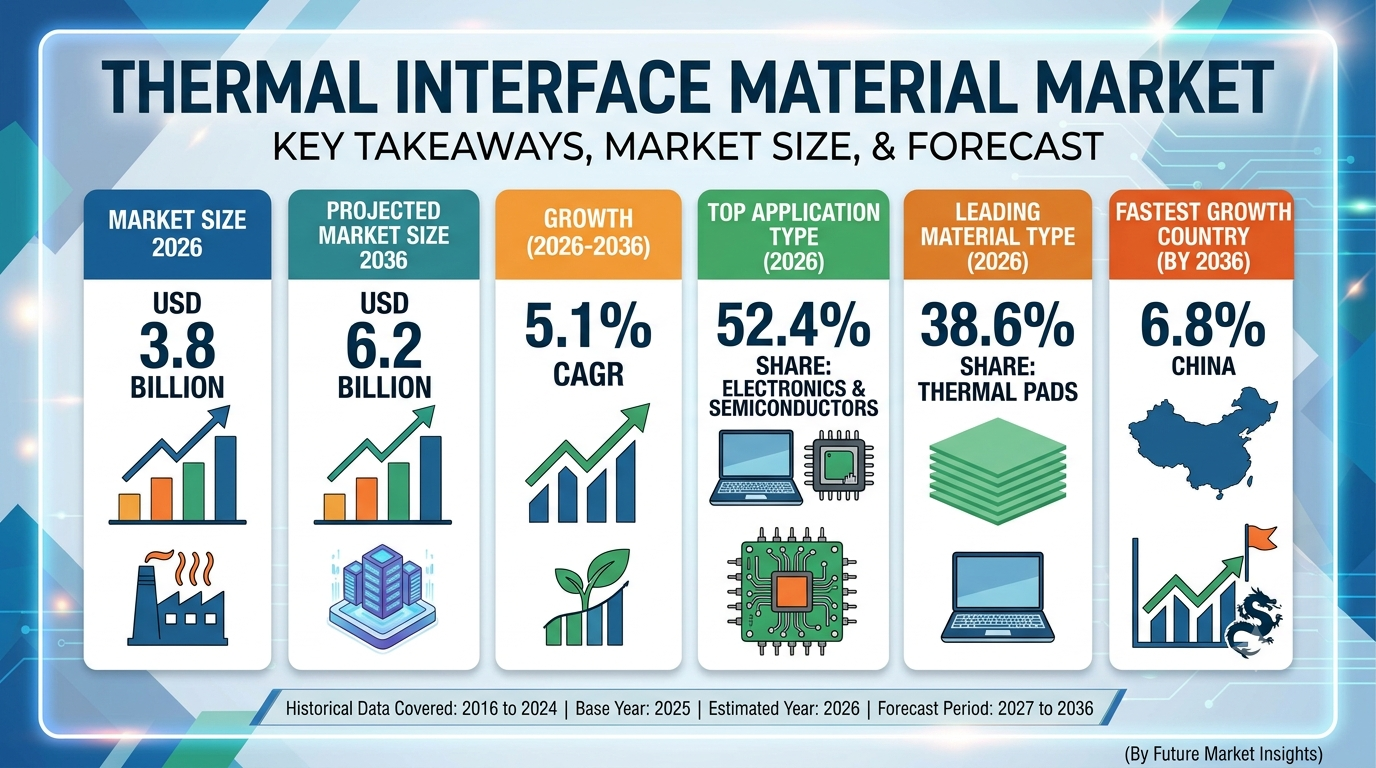

The global thermal interface materials (TIM) market is projected to witness strong expansion over the next decade, supported by tightening performance demands for compact electronics and rising electric vehicle (EV) production across the globe. The market is expected to grow steadily, reaching approximately USD 6.2 billion by 2036, up from USD 3.8 billion in 2026, registering a CAGR of 5.1%, according to the latest analysis by Future Market Insights (FMI).

Market growth is being shaped by increasing government and industry standards for electronic reliability, growing consumer demand for high-performance devices, and rapid adoption of advanced automotive technologies. Thermal interface materials have evolved from simple insulating components into critical performance elements essential for the reliable operation of advanced processors, power electronics, and battery systems. While traditional thermal pastes continue to secure high-performance installations, manufacturers are increasingly integrating specialized materials such as thermal pads, tapes, and phase change materials to comply with modern design expectations and improve heat dissipation outcomes.

Thermal Interface Materials Market Snapshot (2026–2036)

- Market value (2026): USD 3.8 billion

- Market size outlook toward 2036: USD 6.2 billion

- Forecast CAGR: 5.1%

- Dominant application category: Electronics and Semiconductor (52.4% share in 2026)

- Fastest-growing country segment: China (6.8% CAGR through 2036)

- Key demand segments: Thermal pads (38.6% share) and Thermal paste (28.4% share)

- Primary demand channel: Electronics Manufacturing and OEM Integration

Momentum in the Market

Beginning from steady regional adoption levels, the thermal interface materials market demonstrates accelerated growth throughout the forecast period as electronics and systems reliability becomes paramount. Between 2026 and 2036, expanding semiconductor capacity and data center equipment upgrades are expected to significantly boost demand for integrated thermal management solutions. Increasing component density and higher processing speeds are encouraging electronics manufacturers and automakers to prioritize occupant and hardware protection technologies.

From 2036 onward, innovation in adaptive thermal formulations and integration with next-generation automated production systems is expected to further strengthen market expansion. Advanced formulations capable of adapting thermal performance based on operating cycles and high heat fluxes are emerging as key differentiators in new hardware architectures.

The Reasons Behind the Market’s Growth

Demand for thermal interface materials is rising due to multiple structural and technological factors reshaping the global hardware and industrial ecosystem.

- Miniaturization and Electronics Upgrades: The ongoing shift toward compact, high-power electronics requires advanced thermal dissipation. TIMs prevent localized overheating in tightly packed processor layouts.

- Growing EV and Battery Manufacturing: Rapid expansion of electric vehicle powertrain assemblies and battery modules drives large-scale OEM adoption of stable thermal control layers.

- Data Center and Telecom Expansion: The roll-out of high-speed telecommunications hardware and intensive computing servers increases the need for high-performance material qualification.

- Rising Hardware Longevity Standards: Manufacturers prioritize high-quality formulations to extend component lifespan, reduce failure rates, and comply with strict corporate quality control standards.

Top Segment Application Type

Electronics and Semiconductor Leads Market Demand

Electronics and semiconductor applications account for the majority of installations, holding a commanding 52.4% share of the application segment in 2026. This dominance is supported by the universal necessity of efficient heat transfer across modern processing units.

Material Type Analysis

- Thermal pads: Represent 38.6% of the market in 2026, reflecting priority on applications requiring conformable materials and easy assembly characteristics.

- Thermal paste: Accounts for 28.4% of market share, suitable for processor cooling and high-performance applications requiring maximum thermal conductivity.

- Thermal tape: Contributes 17.9% of the market, primarily used in consumer electronics and portable device applications requiring efficient adhesive properties.

- Phase change materials: Represent 10.3% of demand, favored for applications requiring adaptive thermal properties and temperature cycling resilience.

- Other materials: Account for the remaining 4.8% of the global market.

Regional Development: Manufacturing Ecosystems Drive Expansion

The global supply chain is evolving into highly specialized fabrication hubs for thermal safety and management components, supported by advanced processing methods and localized material production.

- China: Projected to record the fastest country-level expansion with a 6.8% CAGR through 2036, driven by intense manufacturing scale and local semiconductor activity.

- North America and Europe: Expanding automotive electronics assembly and advanced industrial equipment infrastructure.

- Rest of Asia-Pacific: Highly active electronics manufacturing services (EMS) facilities and consumer electronics production clusters.

Localized manufacturing partnerships between global material suppliers and regional hardware manufacturers are improving cost efficiency while accelerating material technology adoption.

Challenges, Trends, Opportunities, and Drivers

Drivers

- Tightening performance criteria for semiconductor hardware

- Surge in high-capacity electric vehicle production

- Escalating high-speed telecommunication upgrades

- Rising demand for electronics reliability and device longevity

Opportunities

- Smart, phase-adapting thermal interface materials

- Eco-friendly and recyclable TIM formulations

- Low-thickness, high-conductivity custom shapes for specialized microprocessors

- Integration into automated high-volume assembly lines

Trends

- Transition toward advanced processing methods and automated material placement

- Increased reliance on highly conformable thermal pads for complex geometries

- Rising application of phase change chemistry to handle temperature spikes

- Focus on quality-controlled supply chains to prevent raw material bottlenecks

Challenges

- Broader deployment shaped by the availability of specialized raw materials

- Production capacity limitations for complex synthetic formulations

- Cost pressures for entry-level electronics consumer goods

- Strict compliance with evolving international manufacturing environmental standards

Country Growth Outlook

The market’s growth trajectory is closely tied to industrialization and advanced technological integration across major global economies:

- China: Strong manufacturing leadership, high volume consumer electronics hubs, and significant regulatory support for EV ecosystems.

- United States: Expansion of data centers, cloud infrastructure, and aerospace electronics.

- Germany and Japan: Advanced automotive electronics engineering and specialized industrial automation.

- South Korea and Taiwan: Global semiconductor fabrication centers requiring maximum performance TIM validation.

The Competitive Environment

The global thermal interface materials market is moderately consolidated, with primary materials technology providers competing through formulation innovation, localized manufacturing, and regulatory compliance.

Leading companies invest heavily in creating high-conductivity polymers, lightweight structures, and automated dispensing compatible variants. They actively form partnerships with regional OEMs and semiconductor foundries to secure long-term supply agreements and accelerate custom material development cycles.

Future Outlook: Toward Intelligent and Safer Mobility

The thermal interface materials market is entering a transformative decade shaped by electrification, extreme computational power, and stricter performance expectations. Future TIM formulations are expected to function as highly integrated, reliable layers operating alongside complex cooling setups like liquid cold plates and direct-to-chip systems. As global electronic architectures mature and heat flux demands intensify, thermal interface materials will remain central to achieving durable, highly efficient, and safer technology ecosystems.

Report Link: https://www.futuremarketinsights.com/reports/thermal-interface-materials-market

- Art & Craft

- Causes & Effect

- Dance & Music

- Health & Fitness

- Food & Wellness

- Historic Places

- Homes & Gardening

- Literature & Knowledge

- Science and Technology

- Social Networking

- Social Commerce

- Party & Celebration

- Religion & Festivals

- Shopping & Vendors

- Sports & Games

- Film & Theater

- Digital Creators & Community

- Influencer CCC

- Corporate & Collaboration

- Startup & Scope

- Investment & Growth

- VC & Angel Investors

- Agriculture & farmers

- Nature & Universe

- News & Media

- Real Estate & Property

- Artificial Intellegence

- Political Coverage

- Winners & Loosers